Global Markets Sunday News

AI continues to lead the way

European stock markets experienced a particularly volatile week. At the start of the week, they surged sharply on hopes for peace in the Middle East and falling oil prices. However, the indices were then dragged down again by new U.S. attacks, which called the ceasefire into question. Furthermore, Tehran has not yet signed the memorandum of understanding.

Wall Street, on its own, embarked on a new rally and continues to be buoyed by AI stocks. With new developments in the Strait of Hormuz, volatility is likely to continue to dominate the picture.

Highs & Lows of the Week

Tops

Flex +55,04 %: The stock rose sharply following the announcement of the annual results. The spin-off of the cloud and energy infrastructure division—where the value potential associated with data centers is concentrated—was a particular source of excitement.

Brembo +32,38 %: Shares in the automotive supplier, which specializes in braking systems, surged following the release of its first-quarter results. A key factor in this was the more positive outlook for 2026, which helped dispel the skepticism that had arisen after the company presented a scenario in March predicting stagnant business performance. Several analysts revised their ratings upward.

Soitec +34,97 %: Despite still modest gains and extreme volatility, the market is betting on a cyclical recovery and the Edge & Cloud AI sector. Soitec stock is the big AI hope on the French market. Since January 1, the stock has posted gains of a staggering 550%.

Datadog +42,43 %: The market reacted positively to first-quarter results that far exceeded expectations and a significant upward revision of the 2026 targets. The company is benefiting from demand in the AI and cloud observability sectors.

Umicore +27,01 %: The Belgian recycling company is riding a wave of success following strong quarterly results, driven by metals and an upward revision of its 2026 EBITDA forecast to approximately €1 billion. Berenberg has raised its price target from €21.60 to €23.50.

Hochtief +20,08 %: The stock continues its upward trend in the infrastructure/data center sector. The market is responding positively to the group’s future prospects and margins.

Corning +18,12 %: The stock continues its upward trend in the infrastructure/data center sector. The market is responding positively to the group’s future prospects and margins.

Prysmian +18,84 %: The momentum continues to be driven by the first quarter of 2026 and the structural trend toward electrification. Furthermore, the market is responding positively to growth in the cable business. The company’s CEO has stated that Prysmian is on the verge of finalizing long-term contracts with hyperscalers.

Continental +10,13 %: The first-quarter results provided some reassurance, with sales figures exceeding expectations, the reaffirmation of forecasts, and margin increases at Tire/ContiTech.

Logitech +9,85 %: With its latest quarterly results, the group has demonstrated that it is still capable of delivering positive surprises. Given the relatively unspectacular demand, its business performance can be considered solid.

Safran +4,87 %: Cyclical stocks have benefited from the prospect of a return to normalcy in the Middle East, which bodes well for both the global economy and the engine manufacturer’s customers, such as airlines.

Compagnie Financière Richemont +6,67 %: Another cyclical indicator. The luxury goods sector is benefiting from the (relative) easing of tensions in Iran and is showing signs of recovery. This sector depends both on the travel industry and on wealthy customers in the Gulf states.

Flops

Rovi -20,84 %: The Spanish pharmaceutical company was hit hard following a sharp drop in first-quarter profits and, in particular, the downward revision of its 2026 forecasts due to delays in contract development and manufacturing (CDMO), its heparin business, and price pressures.

Zoetis -27,44 %: The reasons for the decline in the stock price include a disappointing first quarter and the downward revision of annual forecasts against the backdrop of pronounced weakness in the U.S. pet market.

CSG -0,02 %: The week was dominated by short seller Hunterbrook’s attack on the Czech defense contractor, whose business model was called into question. CSG rejected the allegations but was unable to completely halt the decline in its stock price.

Alcon -15,54 %: Quarterly sales were not exactly impressive. The leading contact lens manufacturer fell short of expectations in terms of sales and, despite raising its profit forecast, cites pressure on margins.

Davide Campari -10,79 %: The market has punished the company for a weak quarter in which it failed to meet expectations. A decline in organic revenue raises new questions about the performance of the spirits business.

Coupang -17,53 %: The decline in share price is attributable to another net loss in the first quarter and the sharp drop in adjusted EBITDA, despite continued revenue growth.

Tops / USA

Centene +27,55 %, Bloom Energy +25,67 %, NXP Semiconductor +20,98 %, Intel +20,69 %: These companies’ quarterly results were well received by the market this week.

Flops/ USA

Rambus -29,34 %, Teradyne -17,38 %, Robinhood -13,04 %, SoFi Technologies -10,9 %: The companies’ financial results did anything but please investors.

Brown-Forman -9,75 %: The owner of the Jack Daniel’s brand has called off the merger with its French competitor, Pernod Ricard. The deal could have given the already struggling stock a boost, but the market reacted unfavorably on the European side as well.

Raw materials

Energy

The situation in the Strait remains unstable, but the market remains optimistic nonetheless. After all, direct or indirect negotiations are underway between the U.S. and Iran. Against this backdrop, oil prices fell. Brent crude dropped to around $100, and U.S. WTI crude also fell to $95. However, this decline is quite fragile given the still significant tensions in the Middle East. On Friday, fighting broke out again near the Strait of Hormuz. Donald Trump downplayed these incidents and reaffirmed that the ceasefire remains in place. There are only two possible outcomes for oil prices: If a ceasefire is signed and the Strait of Hormuz reopens, prices are likely to fall. However, if negotiations drag on, prices will remain high.

Metals

The price of gold continues to rise and, just like the price of oil, fluctuates in line with developments in the Middle East. A potential peace agreement would significantly ease fears of rising energy prices. If inflation is brought under control, it would be easier for the Federal Reserve to cut interest rates. As is well known, gold becomes more attractive when interest rates fall, since the metal does not generate a direct return for investors. However, the rise in the price of gold is being limited by ongoing uncertainties. Iran is currently refusing to reopen the Strait of Hormuz. As a result, the price of one troy ounce of gold rose to $4,730. Silver followed this trend, rising 7% to $81. In London, copper posted its best weekly performance since January. A ton of copper is priced at $13,393 (3-month futures). Global supply is extremely tight, which is driving the price higher. On the one hand, the mining company Freeport-McMoRan is delaying the return to full capacity at its Grasberg mine in Indonesia, which is one of the most important in the world. On the other hand, blockades in the Strait of Hormuz are causing bottlenecks in the supply of sulfuric acid, which is essential for copper production.

Agricultural commodities

Wheat, corn, and soybeans took a breather in Chicago. Prices fell over the past week. Wheat is currently trading at approximately 614 cents (July 2026 contract). Market participants are closely monitoring the weather outlook in the U.S., where drought conditions prevail in wheat-growing regions. The upward trend in cocoa is accelerating, with prices rising by about 20% this week. Uncertainties regarding harvests in West Africa are increasing due to a fertilizer shortage.

Macroeconomics

Market sentiment

Another positive surprise from the U.S. job market: 115,000 new jobs were created in the U.S. economy in April. That is significantly more than the 65,000 jobs forecast by economic experts. The unemployment rate, however, remained at 4.3% as expected. This marks the first time in a year that the U.S. economy has achieved job growth for two consecutive months. The jobs report aligns well with the data from recent weeks: The U.S. economy is doing well, the labor market remains solid, and the Fed can focus on the other part of its mandate—inflation. Since the last Federal Reserve meeting, the question is no longer when the Fed will cut interest rates, but rather when the opportunity will arise to raise them again. In this environment, interest rates remain near their annual highs. The yield on 10-year U.S. Treasuries is around 4.4%.

Cryptocurrencies

Bitcoin has gained 1.3% since Monday and is approaching the $80,000 mark. Bitcoin spot ETFs continue to see massive inflows: these exchange-traded products recorded net inflows for the sixth consecutive week. During this period, $3.5 billion in new funds was raised. This brings the assets under management in Bitcoin spot ETFs to $107 billion, which corresponds to 6.67% of all Bitcoins currently in circulation. At the moment, the leading cryptocurrency is continuing its trend from April. Bitcoin is trading with a similar level of volatility to tech stocks. However, while Bitcoin’s ups and downs used to be more pronounced, investors now seem to be focusing more on AI than on cryptocurrencies. As a result, Bitcoin’s volatility is no longer nearly as dramatic as it used to be. As for other cryptocurrencies, Ether (ETH) fell by 2% to approximately $2,200. Solana (SOL) rose by 5% to $88, and XRP remains unchanged at $1.38.

Outlook

Artificial intelligence and the Strait of Hormuz: these are currently the two dominant topics. Beyond that, there is hardly anything else on investors’ minds right now. The bottom line is that AI has taken center stage and helped push U.S. indices to new highs. Wall Street posted gains for the sixth consecutive week, buoyed by an excellent earnings season.

Next week, we may be able to discuss other topics as well. First up is some economic data, including a series of figures on U.S. inflation. After that, all eyes will surely turn to China, where Donald Trump is expected for a two-day visit on Thursday and Friday. The conflict in Iran, however, is likely to remain a focus.

We wish you all a wonderful weekend.

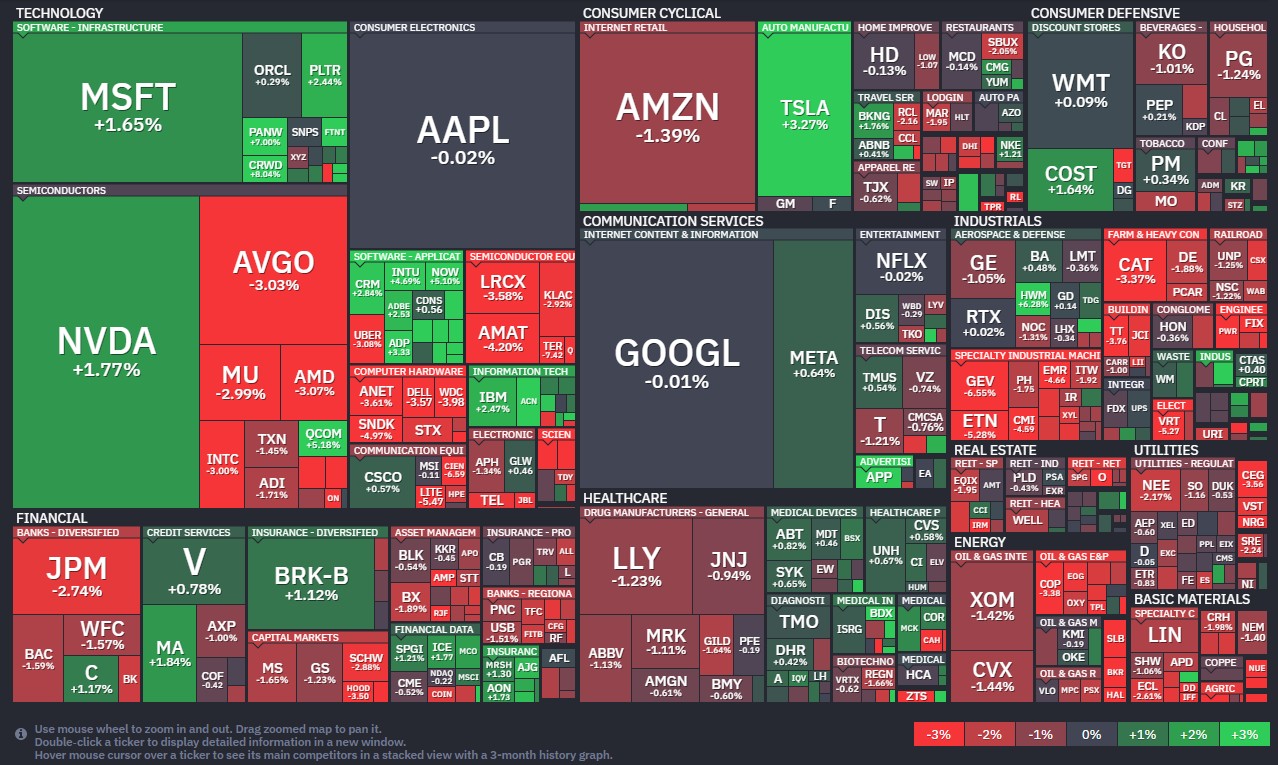

S&P 500 Heatmap

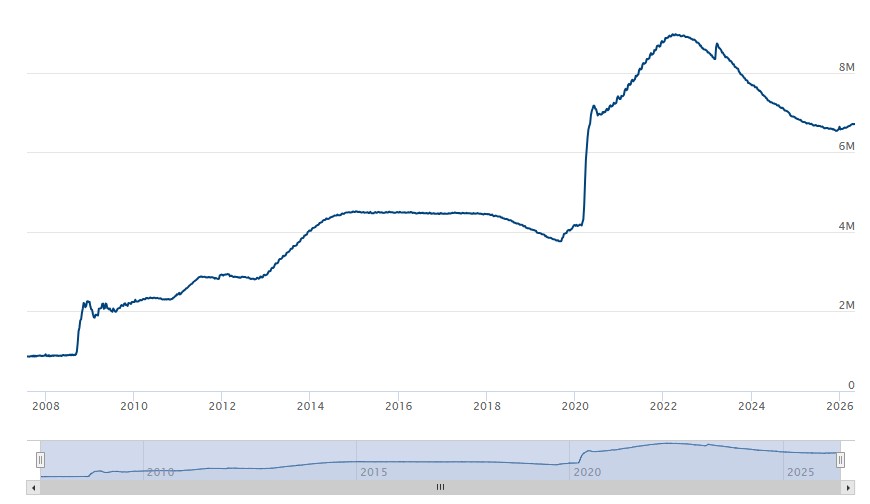

S&P 500 performance in 2025

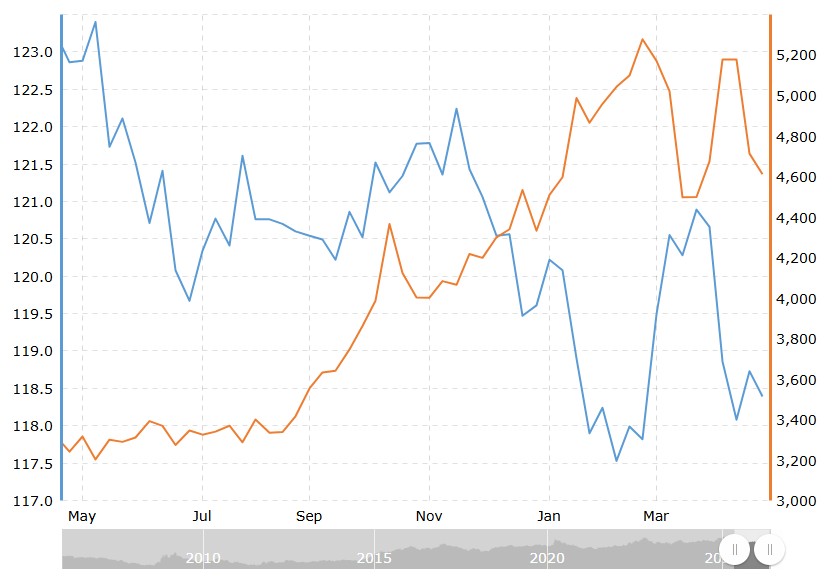

U.S. bond yield

2-year US bond yield

10-year US bond yield

Correlation between the price of gold and the US dollar